Introduction to the Emission Control Catalysts Market

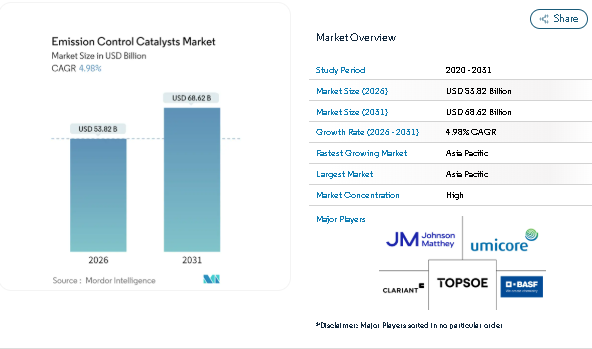

The Emission Control Catalysts Market has become a critical component in reducing air pollution from vehicles and industrial operations. Valued at USD 51.27 billion in 2025, the market is expected to grow from USD 53.82 billion in 2026 to reach USD 68.62 billion by 2031, at a CAGR of 4.98%. This growth is largely driven by tightening emission regulations across key markets, continued internal-combustion engine production in emerging economies, and ongoing improvements in catalyst technology.

Emerging Trends in the Emission Control Catalysts Market

Tightening Global Emission Standards

Stringent emission regulations are the primary driver of the Emission Control Catalysts Market. Policies such as Euro 7 in Europe, China VI, India BS VI, and North America’s Tier 4 off-road rules are compelling automakers and industrial operators to adopt advanced catalysts. Gasoline particulate filters, Diesel Oxidation Catalysts (DOC), Selective Catalytic Reduction (SCR), and Three-Way Catalysts (TWC) are becoming standard in new vehicles and industrial installations.

Rebound in Vehicle Production

Global production of light-duty and heavy-duty vehicles is recovering after recent disruptions. This increase in output directly translates to higher demand for emission control catalysts, as manufacturers integrate advanced after-treatment systems to meet regulations.

Public Health and Air-Quality Concerns

Air pollution in major cities, particularly in China and India, is now a public-health priority. Governments are introducing low-emission zones, strict inspection regimes, and incentives for cleaner technologies. Catalysts capable of converting over 99% of harmful pollutants are increasingly seen as essential tools for reducing health risks from PM2.5 and NOx exposure. This trend ensures consistent adoption across both automotive and stationary sectors.

Industrial and Power Sector Adoption

Stationary applications in power generation and industrial operations are experiencing accelerated uptake. Coal-fired plants, gas turbines, and large-scale industrial generators are installing SCR units and oxidation catalysts to comply with stricter NOx and CO limits. The industrial adoption trend, growing at a faster rate than automotive in some regions, provides diversification for the market and a steady source of long-term demand.

Get expert-backed research and strategic insights with complete analysis here - https://www.mordorintelligence.com/industry-reports/emission-control-catalysts-market?utm_source=premiebook

Market Segmentation in the Emission Control Catalysts Market

By Metal:

-

Platinum

-

Palladium

-

Rhodium

-

Other Metals (Vanadium, Cu-Zn, etc.)

By Technology:

-

Three-Way Catalysts (TWC)

-

Diesel Oxidation Catalysts (DOC)

-

Diesel/GPF Particulate Filters (DPF/GPF)

-

Selective Catalytic Reduction (SCR)

-

Lean NOx Traps & NSC

-

Emerging Nano-Structured Catalysts

By Application:

-

Mobile Emission Control

-

Stationary Emission Control

By End-User Industry:

-

Automotive

-

Industrial

-

Other End-User Industries (Aerospace, Power Generation, etc.)

By Geography:

-

Asia-Pacific

-

China

-

India

-

Japan

-

South Korea

-

ASEAN Countries

-

Rest of Asia-Pacific

-

North America

-

United States

-

Canada

-

Mexico

-

Europe

-

Germany

-

United Kingdom

-

France

-

Italy

-

Rest of Europe

-

South America

-

Brazil

-

Argentina

-

Rest of South America

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

Rest of Middle East and Africa

For a more tailored understanding, view the localized Japanese edition alongside the global market breakdown - https://www.mordorintelligence.com/ja/industry-reports/emission-control-catalysts-market?utm_source=premiebook

Key Players in the Emission Control Catalysts Industry

-

Clariant: Known for high-performance catalyst solutions and sustainable material management.

-

Umicore: Invests in AI-guided material discovery to improve catalyst efficiency and reduce development timelines.

-

Johnson Matthey: Offers extensive automotive and industrial catalyst portfolios.

-

Haldor Topsoe A/S: Focused on SCR and oxidation catalysts for stationary and mobile applications.

-

BASF: Implements additive manufacturing to optimize catalyst structure and performance.

Conclusion

The Emission Control Catalysts Market is expected to grow steadily through 2031, driven by regulatory compliance, vehicle production, and industrial adoption. While electrification gradually reduces demand in some areas, hybrids, commercial vehicles, and industrial applications sustain growth. Trends like metal substitution, nano-structured catalysts, and advanced manufacturing help manage costs and efficiency. Asia-Pacific leads geographically, with North America and Europe focused on technology adoption, and emerging regions catching up. Emission control catalysts remain vital for public health, industrial compliance, and automotive emission reduction.